Aptiv has solid credentials and meaningful exposure to autonomous driving and vehicle electrification megatrends.

Aptiv’s deep linkages in automotive industry help it in navigating through tough times, and the latest equity raise point to investor confidence as well as potential M&A action.

Even after the recent recovery, Aptiv offers comfort in valuations when compared with listed automotive vendors as well as with privately-held companies.

Recent collaborations by self-driving startups point to increasing opportunities at intersections of industries like automotive technology and food delivery.

Accordingly, Aptiv’s valuations should breakaway from traditional automotive industry and should mimic technology players in the long term.

Automotive technology player Aptiv (APTV) has reclaimed much of the ground it lost in March following coronavirus outbreak. While the liquidity fueled rally has lifted all boats, Aptiv’s deep linkages in the industry and a clear handle on costs limit downside. At the same time, its presence in emerging profit pools like autonomous driving and vehicle electrification offer headroom for further growth.

Autonomous driving technology and more

Formerly known as Delphi Automotive, Aptiv has its roots going back to General Motors (GM) and thus, its human capital has always had the advantage of working on the latest technology. The spinoff of powertrain and aftermarket business in 2017 in the form of Delphi Technologies (DLPH) left the legacy business with a highly focused portfolio in two areas:

Signal and Power Solutions: Vehicle electrical systems, wiring and cable assemblies, electrical centers, hybrid high voltage, and safety distribution systems. The division contributes nearly 72% of Aptiv’s revenues.

Advanced Safety and User Experience: Advanced software and sensing systems, computing platforms, advanced safety systems and automated driving, user experience and infotainment. The division accounts for nearly 28% revenues of the company.

This shows that Aptiv has well-diversified portfolio that goes beyond autonomous driving and, thus, is placed favorably to navigate troubled waters and the infamous automotive industry cycles.

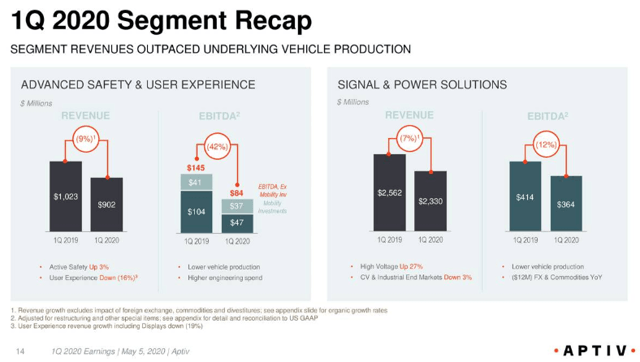

Source: Aptiv’s Q1 2020 Earnings Presentation

An important take away from this image is that revenues grew 3% and 27% for Active Safety and High Voltage components, respectively, even in the current scenario when overall revenues were down. This clearly shows the areas automakers are prioritizing and thankfully, Aptiv stands to benefit by riding two megatrends – autonomous driving and vehicle electrification.

Following the completion of autonomous driving joint venture [JV] with Hyundai (OTCPK:HYMLF), Aptiv has transferred its self-driving business to the JV. The fortunes of active safety and autonomous driving are intertwined, and better traction for active safety business during the first quarter shows that the JV with Hyundai has better days ahead.

From capital preservation to offensive

Meanwhile, Aptiv has taken cognizance of its other businesses that aren’t performing well and has taken steps to reduce its cash outgo. During the quarter, the company intensified austerity measures to further reduce its cost structure and preserve financial health at annualized rate of USD600 million. Important among these are suspension of dividend and lowering in capital expenditures. Other painful but prudent measures include furloughs, temporary layoffs, and cuts in executive pay. This USD600 million translates into an impressive figure of over 4% of Aptiv’s 2019 topline. This is quite impressive in my books.

At the same time, the company bolstered liquidity and was able to make favorable changes in covenant restrictions. In total, Aptiv closed the quarter with liquidity position of USD2.2 billion and further issuance of ordinary and preferred shares is set to boost liquidity by another USD2 billion. During the Q1 results presentation, the management made it clear that its focus is on running operations smoothly, but with the latest equity raise, I suspect Aptiv’s top brass is preparing for some bolt-on acquisitions. Almost invariably, such opportunities present themselves in such tumultuous times.

Source: Aptiv’s Q1 2020 Earnings Presentation

Aptiv expects the current quarter to be more severe in terms of vehicle production declines and these steps are well-timed. For the full year, it expects global light vehicle production to be down around 20-30%.

Converging industries: Opportunity beyond automotive

The coronavirus pandemic has highlighted a highly practical use case of self-driving technology that goes well beyond the traditional automotive industry. While the massive health crisis has somewhat disrupted the uptake of electric vehicles, self-driving vehicles have proved their usability.

In all likelihood, this unfortunate health crisis will be over in the next 12-18 months or so and self-driving vehicles will not be available for mass deployment by that time. Nevertheless, encouraging results through projects such as Baidu’s collaboration with several service providers as well as self-driving startup Nuro’s 3X growth in delivery service demand point to a positive outlook in a not so distant future.

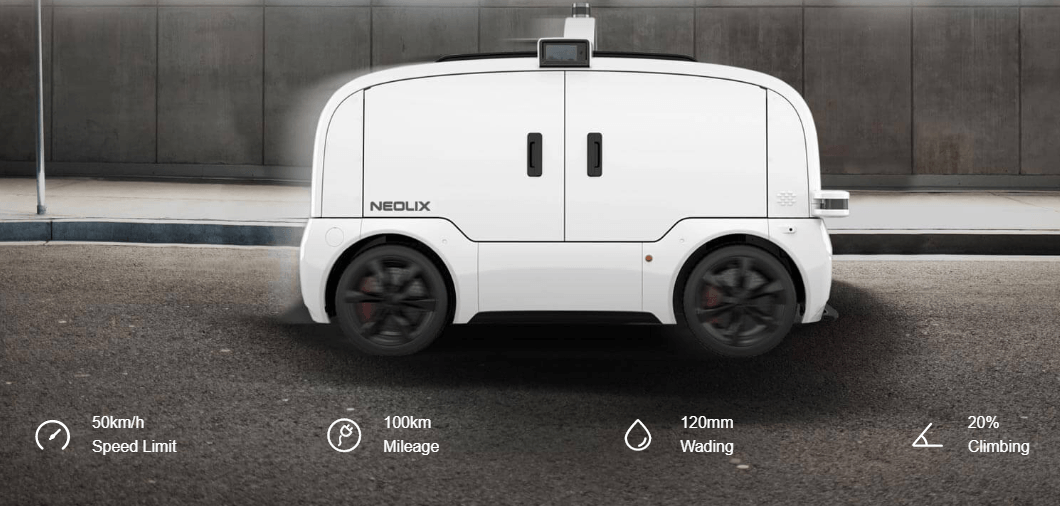

These collaborations point to increasing opportunities at intersections of industries like automotive technology and food delivery. For instance, Baidu’s hardware partner Neolix has designed its unmanned vehicles to perform a range of activities including food delivery, road disinfection, and security robot. While most businesses suffered during the pandemic, Neolix has seen its order book swell to 1,000 units of Level 4-capable delivery vehicles.

Source: Neolix

On similar lines, Nuro – which already counts Kroger (KR) among its clients – is preparing to work with Walmart (NYSE:WMT) and Domino’s Pizza (NYSE:DPZ) for automated delivery services.

Comfort in valuations

After falling in March, Aptiv stock price has captured much of the lost ground, although it is still down 20% from January highs. In terms of revenue and EBITDA growth, the company hasn’t outperformed the industry in recent years. Accordingly, its valuations have stayed range bound. At current levels, it trades at a comfortable P/E ratio of 8.42 on GAAP basis [17.22 on non-GAAP basis]. In contrast, P/E ratios of Magna (NYSE:MGA), BorgWarner (BWA), and LKQ Corporation (NASDAQ:LKQ) are in double digits.

The recent drawdown of revolving credit facility means that Aptiv’s Debt/Equity ratio has increased to 1.29 but considering the circumstances, temporary nature of drawdown, and no major maturities until 2024, it is not alarming.

There are plenty of traditional vendors supplying nuts and bolts to automakers but few listed players work on cutting edge technologies the way Aptiv does. Bigger players like Alphabet (NASDAQ:GOOGL), Uber (UBER), and Tesla (TSLA) are front runners in self-driving technology but they have far too many and powerful factors at play overshadowing their technology expertise. Several other notable players such as Argo AI and Aurora are privately held.

Amazon’s recent acquisition of Zoox for USD1.2 billion offers some yardstick in this regard. Going by Zoox’s annual revenue of around USD360 million, the acquisition price tag translates to EV/Sales multiple of 3.33. This assumes an unlikely scenario of no debt on the books of Zoox. Since Zoox is privately-held, we are not sure about its debt levels but even if we consider small amount, this multiple stands to go up further. On the other hand, Aptiv trades at EV/Sales multiple of just 1.81.

As mentioned above, Aptiv has a diversified portfolio beyond the autonomous driving business which makes direct comparison with Zoox ineffective. Nevertheless, it is fair to say that Aptiv – one of the few listed companies with a critical size in autonomous driving – trades at comfortable valuations. As the race to autonomous driving heats up going forward, it leaves enough room for the stock to run up.

Bottom line

McKinsey forecasts that autonomous vehicles will account for nearly 66% of total passenger kilometers in 2040 and while this figure is huge, it represents only the passenger bit of the equation. The other parts of the puzzle are autonomous last-mile delivery of food and medicines by drones and ground vehicles. A quick Google search tells me that this segment is estimated to be worth USD11 billion by next year. Now, this includes aerial deliveries as well, but it is reasonable to conclude that the figure for ground vehicles is also not small. These market adjacencies are effectively new revenue pockets for software and technology players like Aptiv.

This market understanding is useful for investors in two ways. Firstly, the opportunity size for players like Aptiv is multi-fold considering the scope in various industries as well as recurring nature of revenues. Secondly, it would be wrong to value Aptiv by the standards of automotive industry going forward. At least a portion of its top line and margins will start growing like software technology companies in the coming years.

In conclusion, it is fair to say that Aptiv has a long runway ahead with meaningful exposure to twin megatrends of autonomous driving technology and vehicle electrification. Its technology credentials are already established through the JV with Hyundai and while the coronavirus pandemic has temporarily thrown the industry out of gear, the long-term direction remains intact. While I believe the stock isn’t expensive at current levels to nibble into, we are not out of woods yet and a second wave of infections could offer much better price levels to go full speed ahead. In any case, Aptiv deserves to be a part of long-term portfolios to get above-market returns.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Source: seekingalpha.com

GIPHY App Key not set. Please check settings